flowchart TB ledger["ledger events<br/>source of truth"] fills["fills<br/>execution rows"] trades["trades<br/>closed round trips"] equity["equity rows<br/>portfolio value"] metrics["summary metrics<br/>formulas over results"] ledger --> fills fills --> trades ledger --> equity trades --> metrics equity --> metrics

ledgr records a backtest as accounting evidence first and summary metrics second.

The useful reading order is:

- ledger events say what actually filled;

- fills are execution rows derived from those events;

- trades are only the fill rows that close quantity;

- equity rows value the portfolio through time;

- summary metrics are formulas over those public result tables.

That order matters. A strategy can open a position without closing it. That run has fills and equity exposure, but zero closed trades. In that case n_trades = 0 and win_rate = NA are correct, not missing data.

Prerequisites

Inspection Surfaces

Use the narrowest inspection surface that answers the question:

| Question | Public surface | Shape |

|---|---|---|

| What happened at a glance? | print(bt) |

printed run header with final equity |

| What are the standard metrics? | summary(bt) |

printed interpretation; returns bt invisibly |

| What metric values can code consume? | ledgr_compute_metrics(bt) |

list-like ledgr_metrics object with raw numeric values |

| What rows value the portfolio? | ledgr_results(bt, what = "equity") |

classed tibble |

| What executed? | ledgr_results(bt, what = "fills") |

classed tibble |

| What closed quantity? | ledgr_results(bt, what = "trades") |

classed tibble |

| What did the event ledger record? | ledgr_results(bt, what = "ledger") |

classed tibble |

| How do stored runs compare? | ledgr_run_compare(snapshot, run_ids = ...) |

classed comparison tibble |

| What did a sweep candidate summarize? |

ledgr_sweep() result rows |

classed sweep tibble |

| What context was stored by promotion? |

ledgr_promotion_context(bt) or ledgr_run_promotion_context()

|

nested list |

The result-table helpers return structured objects. Their print methods may format timestamps for readability, but as_tibble() gives raw columns for programmatic use. The stable programming contract is the column meaning, not the number of rows: a valid run can have zero fills, zero closed trades, or a final open position.

Two things are not in the standard result tables.

final_equity is not a field in the ledgr_compute_metrics() list. Read it from the last equity row, from print(bt), from comparison rows, or from sweep rows.

There is no committed ledgr_results(bt, what = "features") table. Feature values are inspected at pulse time with ledgr_pulse_snapshot() or through sweep/precompute provenance, not through a persisted feature-result table accessor.

Metric assumptions are inspectable through ledgr_metric_context(). Use it on a backtest, ledgr_metrics object, comparison table, sweep result table, or promotion context to see the risk-free-rate and annualization context that produced that surface.

A Tiny Run

Use a five-bar in-memory fixture so the accounting can be checked by hand. OHLC values are equal per bar so the example focuses on accounting arithmetic; real bars use the same code with ordinary intra-bar movement. This article uses ledgr_backtest() as a compact fixture helper for accounting examples. The canonical research workflow remains: snapshot -> ledgr_experiment() -> ledgr_run().

bars <- data.frame(

ts_utc = as.POSIXct("2020-01-01", tz = "UTC") + 86400 * 0:4,

instrument_id = "AAA",

open = c(100, 101, 105, 106, 106),

high = c(100, 101, 105, 106, 106),

low = c(100, 101, 105, 106, 106),

close = c(100, 101, 105, 106, 106),

volume = 1

)

one_day_strategy <- function(ctx, params) {

targets <- ctx$flat()

if (ledgr_utc(ctx$ts_utc) == ledgr_utc("2020-01-01")) {

targets["AAA"] <- 1

}

targets

}

bt <- ledgr_backtest(

data = bars,

strategy = one_day_strategy,

initial_cash = 1000,

run_id = "accounting_example",

cost_model = ledgr_cost_zero()

)The strategy asks to hold one share on the first pulse and then returns to flat. In these examples, decisions fill at the next open. The buy therefore fills on the second bar, and the exit fills on the third bar.

Timing, Spread, And Fees

Timing and cost are separate execution steps. ledgr_timing_next_open() decides where a target change can fill: the next available open after the strategy decision. A cost model then resolves the proposed fill price and explicit fee. Strategies do not receive cost state, and cost models do not change side, quantity, instrument, or execution timestamp.

ledgr_cost_spread_bps() uses a quoted bid/ask-spread convention. A buy crosses half the quoted spread above the reference open: open * (1 + spread_bps / 20000). A sell crosses half below it: open * (1 - spread_bps / 20000). For the same reference price, a buy/sell round trip therefore crosses approximately spread_bps basis points before explicit fees.

spread_bps <- 25

reference_price <- 100

buy_cross <- reference_price * (1 + spread_bps / 20000)

sell_cross <- reference_price * (1 - spread_bps / 20000)

round_trip_bps <- (buy_cross - sell_cross) / reference_price * 10000

round(round_trip_bps, 6)

#> [1] 25Price transforms and explicit fees are different. ledgr_cost_spread_bps() changes the fill price. ledgr_cost_fixed_fee() and ledgr_cost_notional_bps_fee() add values to the fill fee column after any price transforms have resolved.

Target risk, timing, and cost are separate layers. A risk_chain can transform validated strategy target quantities before fill proposals exist. The timing model decides which bar is used for execution. The cost model then adjusts price and fee on the accepted fill proposal; it does not decide whether a target is affordable or liquid.

example_cost_model <- ledgr_cost_chain(

ledgr_cost_spread_bps(25),

ledgr_cost_fixed_fee(0.50),

ledgr_cost_notional_bps_fee(1)

)

ledgr_cost_steps(example_cost_model)

ledgr_cost_describe(example_cost_model)What costs do not model

Cost models are deterministic research assumptions over accepted fill proposals. They do not implement liquidity or capacity limits, financing, transaction-cost analysis, taxes, OMS lifecycle behavior, or broker reconciliation. Those are separate future layers, not hidden behavior in the cost API.

Ledger Events

A ledger event is the append-only accounting record written when execution changes cash, positions, or run state. Fills, trades, equity, and metrics are derived views over ledger-backed evidence. The ledger is the most literal view; the friendlier result tables below are derived from these events.

ledger <- ledgr_results(bt, what = "ledger")

ledger

#> # A tibble: 2 x 11

#> event_id run_id ts_utc event_type instrument_id side qty price fee meta_json

#> <chr> <chr> <date> <chr> <chr> <chr> <dbl> <dbl> <dbl> <chr>

#> 1 accounting~ accou~ 2020-01-02 FILL AAA BUY 1 101 0 "{\"cash~

#> 2 accounting~ accou~ 2020-01-03 FILL AAA SELL 1 105 0 "{\"cash~

#> # i 1 more variable: event_seq <int>Fills And Trades

A fill is an execution row: direction, quantity, price, fee, and action. A trade is the subset of fill evidence that closes quantity and realizes P&L. what = "fills" returns execution fill rows. Opening and closing fills both appear here.

fills <- ledgr_results(bt, what = "fills")

fills

#> # A tibble: 2 x 9

#> event_seq ts_utc instrument_id side qty price fee realized_pnl action

#> <int> <date> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <chr>

#> 1 1 2020-01-02 AAA BUY 1 101 0 0 OPEN

#> 2 2 2020-01-03 AAA SELL 1 105 0 4 CLOSEThe important columns are:

| Column | Meaning |

|---|---|

side |

execution direction, such as BUY or SELL

|

qty |

absolute fill quantity |

price |

fill price |

fee |

execution fee charged on the fill |

action |

whether the fill opened or closed quantity |

realized_pnl |

profit or loss booked by closing quantity |

what = "trades" keeps only closed trade rows. That is the table used by n_trades, win_rate, and avg_trade.

trades <- ledgr_results(bt, what = "trades")

trades

#> # A tibble: 1 x 9

#> event_seq ts_utc instrument_id side qty price fee realized_pnl action

#> <int> <date> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <chr>

#> 1 2 2020-01-03 AAA SELL 1 105 0 4 CLOSEThis run has two fill rows but one closed trade row. Counting fills as trades would double-count the round trip.

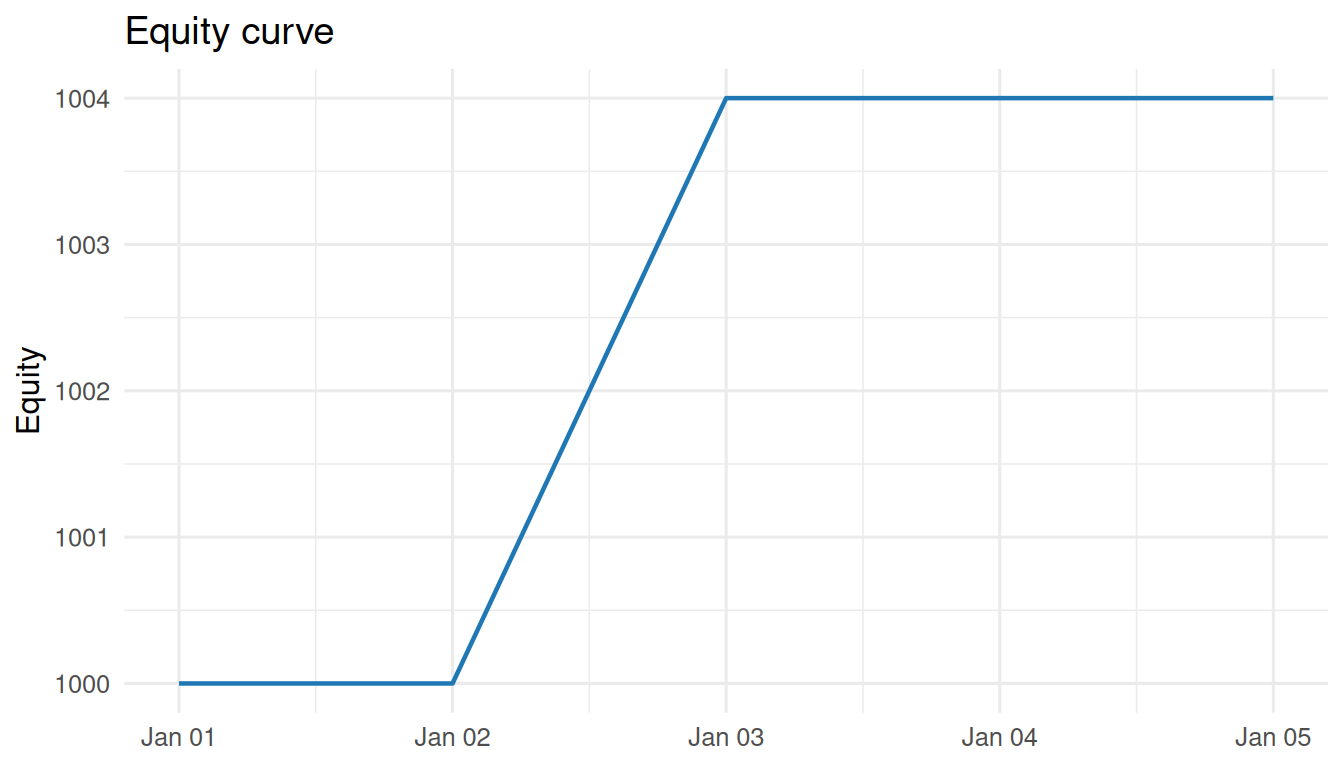

Equity Rows

An equity row values the portfolio at one timestamp. It combines cash, current position value, and total equity, including open-position exposure. The equity curve records portfolio state through time.

equity <- ledgr_results(bt, what = "equity")

equity

#> # A tibble: 5 x 6

#> ts_utc equity cash positions_value running_max drawdown

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 2020-01-01 1000 1000 0 1000 0

#> 2 2020-01-02 1000 899 101 1000 0

#> 3 2020-01-03 1004 1004 0 1004 0

#> 4 2020-01-04 1004 1004 0 1004 0

#> 5 2020-01-05 1004 1004 0 1004 0Open positions affect positions_value and therefore equity even before any trade closes. Realized P&L belongs to closed quantity; open-position gains and losses stay in the equity curve until a closing fill realizes them.

ggplot2::ggplot(equity, ggplot2::aes(x = ts_utc, y = equity)) +

ggplot2::geom_line(linewidth = 0.8, color = "#1f77b4") +

ggplot2::labs(

title = "Equity curve",

x = NULL,

y = "Equity"

) +

ggplot2::theme_minimal(base_size = 12)

Recompute The Metrics

The summary metrics can be recomputed from public result tables.

equity_values <- equity$equity

period_returns <- equity_values[-1] / equity_values[-length(equity_values)] - 1

bars_per_year <- 252

rf_annual <- 0

rf_period_return <- (1 + rf_annual)^(1 / bars_per_year) - 1

excess_returns <- period_returns - rf_period_return

metric_check <- tibble(

total_return =

equity_values[length(equity_values)] / equity_values[1] - 1,

annualized_return =

(1 + total_return)^(

1 / ((length(equity_values) - 1) / bars_per_year)

) - 1,

volatility =

sd(period_returns) * sqrt(bars_per_year),

sharpe_ratio =

mean(excess_returns) / sd(excess_returns) * sqrt(bars_per_year),

max_drawdown =

min(equity_values / cummax(equity_values) - 1),

n_trades =

nrow(trades),

win_rate =

if (nrow(trades) > 0) mean(trades$realized_pnl > 0) else NA_real_,

avg_trade =

if (nrow(trades) > 0) mean(trades$realized_pnl) else NA_real_,

time_in_market =

mean(abs(equity$positions_value) > 1e-6)

)

metric_check

#> # A tibble: 1 x 9

#> total_return annualized_return volatility sharpe_ratio max_drawdown n_trades win_rate

#> <dbl> <dbl> <dbl> <dbl> <dbl> <int> <dbl>

#> 1 0.00400 0.286 0.0317 7.94 0 1 1

#> # i 2 more variables: avg_trade <dbl>, time_in_market <dbl>Those are the same definitions used by summary(bt) and ledgr_compute_metrics(bt). The first public equity row is the initial equity for return calculations. Max drawdown is the maximum peak-to-trough decline in the public equity rows. Time in market is the share of equity rows with absolute positions_value > 1e-6.

ledgr_results() returns persisted result tables: equity, fills, trades, or ledger. There is no what = "metrics" result table. Use summary(bt) for printed interpretation, or ledgr_compute_metrics(bt) when you need the named metric values in code.

This small example uses bars_per_year <- 252 because the bars are daily. ledgr detects bar frequency for ledgr_compute_metrics() and snaps common cadences, such as daily and weekly, to standard annualization constants. Use the detected value if you need an external calculation to match ledgr exactly on non-daily data.

Try it

Change bars_per_year in the recompute chunk from 252 to 365. Which metrics change? Why does total_return stay the same?

Zero Trades Can Be Correct

A flat strategy produces no fills and no closed trades. The result tables still keep their schemas, so downstream code can rely on the same column names.

flat_strategy <- function(ctx, params) ctx$flat()

flat_bt <- ledgr_backtest(

data = bars,

strategy = flat_strategy,

initial_cash = 1000,

run_id = "flat_accounting_example",

cost_model = ledgr_cost_zero()

)

ledgr_results(flat_bt, what = "fills")

#> # A tibble: 0 x 9

#> # i 9 variables: event_seq <int>, ts_utc <date>, instrument_id <chr>, side <chr>,

#> # qty <dbl>, price <dbl>, fee <dbl>, realized_pnl <dbl>, action <chr>

ledgr_results(flat_bt, what = "trades")

#> # A tibble: 0 x 9

#> # i 9 variables: event_seq <int>, ts_utc <date>, instrument_id <chr>, side <chr>,

#> # qty <dbl>, price <dbl>, fee <dbl>, realized_pnl <dbl>, action <chr>

ledgr_compute_metrics(flat_bt)[c("n_trades", "win_rate", "avg_trade")]

#> $n_trades

#> [1] 0

#>

#> $win_rate

#> [1] NA

#>

#> $avg_trade

#> [1] NAwin_rate and avg_trade are NA because there are no closed trade rows to evaluate. That is different from a zero percent win rate, which would mean there were trades and none of them were profitable.

Open Positions And Final-Bar Targets

An open-only run is also valid. It has an opening fill and equity exposure, but no closed trade rows. The unrealized result belongs in equity, not in realized_pnl.

open_only_strategy <- function(ctx, params) {

targets <- ctx$flat()

targets["AAA"] <- 1

targets

}

open_bt <- ledgr_backtest(

data = bars,

strategy = open_only_strategy,

initial_cash = 1000,

run_id = "open_accounting_example",

cost_model = ledgr_cost_zero()

)

ledgr_results(open_bt, what = "fills")

#> # A tibble: 1 x 9

#> event_seq ts_utc instrument_id side qty price fee realized_pnl action

#> <int> <date> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <chr>

#> 1 1 2020-01-02 AAA BUY 1 101 0 0 OPEN

ledgr_results(open_bt, what = "trades")

#> # A tibble: 0 x 9

#> # i 9 variables: event_seq <int>, ts_utc <date>, instrument_id <chr>, side <chr>,

#> # qty <dbl>, price <dbl>, fee <dbl>, realized_pnl <dbl>, action <chr>

ledgr_compute_metrics(open_bt)[c("n_trades", "win_rate", "avg_trade")]

#> $n_trades

#> [1] 0

#>

#> $win_rate

#> [1] NA

#>

#> $avg_trade

#> [1] NAA final-bar target under a next-open fill model can also be valid research input while producing no fill. There is no later bar available for execution, so ledgr warns and leaves the ledger unchanged for that last target change.

final_bar_strategy <- function(ctx, params) {

targets <- ctx$flat()

if (ledgr_utc(ctx$ts_utc) == ledgr_utc("2020-01-05")) {

targets["AAA"] <- 1

}

targets

}

final_bar_bt <- ledgr_backtest(

data = bars,

strategy = final_bar_strategy,

initial_cash = 1000,

run_id = "final_bar_accounting_example",

cost_model = ledgr_cost_zero()

)

#> Warning: LEDGR_LAST_BAR_NO_FILL: target changed on the final available bar, but the

#> next-open fill model requires a following bar. No fill was emitted for this target

#> change. Check the strategy's final-pulse behavior or extend the snapshot if this trade

#> should be fillable.

ledgr_results(final_bar_bt, what = "fills")

#> # A tibble: 0 x 9

#> # i 9 variables: event_seq <int>, ts_utc <date>, instrument_id <chr>, side <chr>,

#> # qty <dbl>, price <dbl>, fee <dbl>, realized_pnl <dbl>, action <chr>Cleanup

Where Next

-

vignette("metric-contexts-and-conventions", package = "ledgr")covers metric contexts, annualization, and diagnostics. -

vignette("execution-semantics", package = "ledgr")explains why fills happen on the next bar and why the final decision bar cannot fill. -

?ledgr_cost_spread_bpsand?ledgr_cost_fixed_feedescribe public transaction-cost model declarations.